-

1. Management Report 2021

- 1.1 In two minutes

- 1.2 Strategy and value creation

- 1.3 Ferrovial in 2021

- 1.4 Risks

- 1.5 Corporate Governance

- 1.6 Expected Business Performance in 2022

-

Appendix

- Alternative Performance Measures

- Sustainability Management

- Reporting Principles

- European Taxonomy

- Task Force on Climate Related Disclosures

- Scoreboard

- Contents of Non-Financial Information Statements

- SASB Indicators

- GRI Standard Indicators

- Appendix to GRI Standards Indicators

- Glosary of Terms

- Verification Report

-

2. Consolidated Financial Statements 2021

- Consolidated Financial Statements

- Audit Report

BUSINESS LINES

Airports

Airports contributed -EUR254mn to Ferrovial’s equity accounted result in 2021, vs. -EUR439mn in 2020.

- HAH: -EUR238mn in 2021 (-EUR396mn in 2020) due to the impact of COVID-19. In 2021, Ferrovial has not integrated the complete negative result of HAH, following IAS 28, which indicates that if the associate’s share of losses equals or exceeds its share, no further losses will be recognized in its shareholding.

- AGS: -EUR20mn in 2021 (-EUR51mn in 2020) following IFRS28, as of December 2021, Ferrovial has integrated negative results from AGS due to additional shareholder funds injected in June 2021, on the back of the Amend & Extend of its debt facility.

In terms of distributions to shareholders:

- HAH: dividends from Heathrow are not permitted until RAR is below 87.5%. Dividends distributed in 1Q 2020 were GBP100mn (EUR29mn for Ferrovial).

- AGS: has not paid dividends in 2021. No dividends allowed for the duration of the Amend & Extend.

HEATHROW SP (25%, equity-accounted) – UK

COVID-19 & Heathrow’s response

With the recovery of international travel hampered by the Omicron variant in 4Q, Heathrow saw 19.4mn pax travel through the airport in 2021. While Heathrow expects increased demand and further recovery in the sector given recent changes to travel restrictions, in particular in the UK, it recognizes the uncertainties that are evident with the pandemic and the impact this can have on travel policy and consumer confidence. Heathrow has taken steps to protect the business over the previous 2 years and improved the organization’s efficiency and resilience. This provides the platform to look forward with confidence as Heathrow prepares for the recovery with sustainability at the center of its plans.

The safety of colleagues and passengers remains the number one priority. Heathrow’s commitment to its COVID-19 safe program has been recognized externally by the Airports Council International, the CAA and Skytrax.

Despite Heathrow’s operating costs base being c. 95% fixed and semi-fixed, the rapid action taken to reduce cost has resulted in savings of GBP870mn during 2020 and 2021. Many of these cost savings were temporary, including reduced staffing, consolidation of operations, temporary reductions in pay and bonuses and furlough. In Q4, Heathrow started to increase costs again to meet the increase in demand and prepare for ramp up.

The costs initiatives implemented throughout 2020 drove a 8.3% cost reduction in 2021 vs 2020, and 27.8% vs 2019. Similarly, the capital plan remains reduced to preserve Heathrow’s cash position with capex reduced by -31.5% (GBP289mn spent in 2021 vs. GBP422mn in 2020).

Despite a challenging market backdrop, continued confidence and support from its creditors enabled Heathrow to raise GBP1.6bn of debt in 2021. Heathrow SP continues benefiting from a strong liquidity position of GBP4.0bn, providing sufficient liquidity to meet all payment obligations well into 2025 under current base case traffic forecast, or until February 2023 in the extreme no revenue scenario.

Traffic

Passenger numbers were down -12.3% in 2021. Traveling was largely closed in 1Q 2021, however in May, the UK Government implemented a traffic light system for international travel, driven by vaccination advances. Over the summer, Heathrow saw a steady build in passengers as more countries were added to the ‘green list’ and fully vaccinated UK residents could travel more freely. In October, the government moved from the traffic light system to one based on individual vaccination status and in November, flights to the US returned for the first time in 18 months. Later in the month, with the emergence of the Omicron variant, the UK Government reintroduced some travel restrictions.

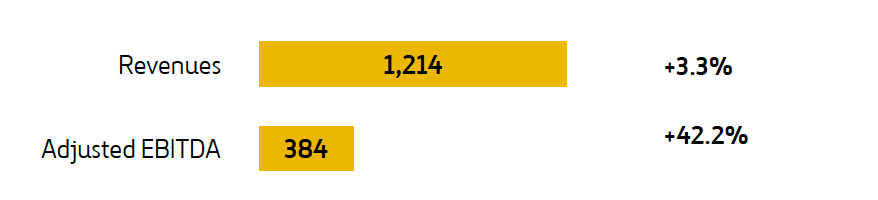

Revenues: +3.3% in 2021 to GBP1,214mn.

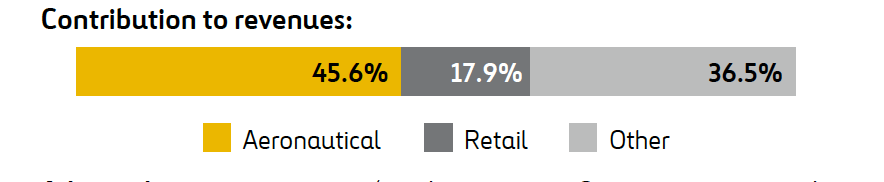

- Aeronautical: -14.4% vs 2020. The decline in aeronautical revenue is predominantly due to reduced pax numbers. Heathrow’s maximum allowable yield for 2021 was £19.36 per passenger, an 18% reduction versus 2020.

- Retail: -7.3% vs 2020, driven by reduced pax. numbers however there was relative resilience in the last quarter as the relaxation of government restrictions allowed the reopening of all our units across Terminals 2, 3 & 5 to take advantage of improved pax. volumes.

- Other revenues: +50.7% vs 2020. Other regulated charges increased by +151.7% predominantly due to revenue under-recovered in prior periods through the Airport Cost Recovery Charge introduced in February 2021 and higher prices for certain Other Regulated Charges (ORCs) such as baggage on the General notice effective from August 2021. Heathrow Express remained flat mainly due to lower passengers offset by a higher yield. Property and other revenue decreased -20.0% showing relative resilience due to agreeing rental payment plans with certain operators.

Adjusted operating costs (ex-depreciation & amortization and exceptional): -8.3% to GBP830mn (GBP905mn in 2020).

Adjusted EBITDA 42.2% to GBP384mn (GBP270mn in 2020).

HAH net debt: the average cost of Heathrow’s external debt was 3.79%, including all the interest-rate, exchange-rate, accretion and inflation hedges in place (2.09% in December 2020).

Heathrow SP reprofiled its swap portfolio and secure interest savings in 2021 while traffic recovers.

Heathrow has deleveraged with inflation due to the fact that impact on RAB (linked to inflation) is higher than the effect on debt linked to inflation with its gearing ratio showing a decrease from 91.7% to 88.4%.

The table above relates to FGP Topco, HAH’s parent company.

Financial Ratios: At December 31st, 2021, Heathrow SP and Heathrow Finance continue to operate within required financial ratios.

As of December 31st, 2021, a forecasting event and trigger event have occurred and are continuing in relation to the historic ICR for senior and junior debt for the year ended December 31st, 2020. As a result, a distribution lock-up remains in place within Heathrow SP and will have no adverse effect on Heathrow SP’s creditors. In August, Heathrow successfully received approval from Heathrow Finance’s creditors to waive the Interest Cover Ratio covenant for the financial year ending on December 31st, 2021.

Heathrow has sufficient liquidity to meet all its forecast needs until at least Feb. 2023 under the extreme stress-test scenario of no revenue, or well into 2025 under its traffic forecast. This liquidity position includes GBP2.6bn in cash resources as well as undrawn debt & liquidity at Heathrow Finance plc as at December 31st, 2021.

Regulatory Asset Base (RAB): at December 31st, 2021, the RAB reached GBP17,474mn (GBP16,492mn in December 2020).

Decarbonizing the aviation sector remains a key priority of Heathrow’s sustainable growth plan.

In February 2022 Heathrow released an update to its sustainability plan, Heathrow 2.0. The plan sets a clear direction for the company to 2030 and beyond, where it will cut emissions and how it plans to do that. Heathrow outlines how it will work in partnership and influence other where it does not directly control emissions emissions.

In 2021 the entire aviation sector globally, committed to net zero by 2050. This commitment will align with the Paris Agreement goal for global warming not to exceed 1.5°C.

In the next regulatory settlement period Heathrow has included GBP188mn of investment in carbon and sustainability improvements in its business plan, which will allow it to deliver the essential projects up to 2026 that will keep it on track to hit its net zero goals in the air and on the ground by 2030.

Following the first delivery of SAF into Heathrow’s main fuel supply in June, a SAF-fuelled ‘perfect flight’ departed from Heathrow to Glasgow in September and further SAF deliveries took place in partnership between airlines and fuel companies, including during COP26 when all British Airways flights between Heathrow and Scottish airports were fuelled with a blend of SAF.

From 2022, Heathrow’s landing charges will include a new financial incentive for airlines to help make SAF more affordable for airlines. The incentive will support 0.5% SAF blend at Heathrow in its first year, climbing steadily in the following years. It will complement a new UK Jet Zero policy the UK Government is planning to introduce.

Through Heathrow’s offsetting partner CHOOOSE, it was offered to companies and passengers the chance to buy SAF. Customers can select to offset their flights by paying for SAF which is used on existing scheduled flights. Heathrow is the first airport in the UK to offer passengers this opportunity.

Key regulatory developments

CAA Initial Proposals for H7 – On 19 October 2021, the CAA’s published its Initial Proposals for the H7 period, setting out the following draft policy positions for the H7 price control:

- A range of cost and revenue forecasts leading to an upper quartile H7 charge of £34.40 (2020 prices) and a lower quartile estimate of £24.50 (2020p prices)

- Three potential capital expenditure plans ranging from GBP1.6bn to GBP3bn.

- A pre-tax WACC range of between 7.09% and 4.38%

- The continued implementation of the GBP300mn RAB adjustment set out in the CAA’s April 2021 decision

- A new traffic risk sharing mechanism and mechanisms to deal with asymmetric risk and cost uncertainty

- Proposals for an ex-ante capital efficiency framework with an incentive of between 20% and 30%

- Movement towards an outcomes-based service quality framework

Heathrow Response and RBP Update 2: Heathrow submitted its response to the CAA’s Initial Proposals on 17 December. Alongside the response it also submitted the second update to Heathrow’s Dec. 2020 Revised Business Plan (RBP).

In the response and RBP Update 2, Heathrow sets out its responses to the CAA’s policy proposals and H7 building block forecasts and provided its updated view of passenger volumes and cost and revenue forecasts for the H7 period. Key updates include:

- An H7 charge of GBP41.95 (2018p) reflecting new forecasts of opex, commercial revenues and a revised passenger forecast of 317.1mn over the H7 period;

- Opportunity to reduce charge to GBP34 if CAA enables deferral of regulatory depreciation beyond H7 by providing a full RAB adjustment;

- A pre-tax WACC of 8.5%;

- A capital plan of GBP4.1bn (2018p), allowing Heathrow to invest in key programmes such as Regulated Security Compliance, the refurbishment of the Terminal 2 baggage system and decarbonization and sustainability;

- A full RAB adjustment of GBP2.5bn to fully implement the CAA’s regulatory framework following the impact of COVID-19;

- Proposed changes to the CAA’s risk sharing mechanism to ensure it reflects the commercial revenue risk inherent in the single till model

The CAA will continue its H7 process through 2022 with the H7 price control due to be implemented in summer 2022. The next step in the process is the publication of the CAA’s Final Proposals, currently due for 2Q 2022.

2022 Airport charges: On 22 Dec., the CAA published its license modifications to set an interim price cap of GBP30.19 (2022, CPI) for 2022. This price cap will be in place until the CAA’s final decision on H7 is published. The CAA has stated that it will perform a ‘true up’ to account for the difference between this interim holding cap and the final H7 decision.

Heathrow Expansion

While Heathrow has paused work to expand the airport during COVID-19, the crisis has shown the pent-up demand from airlines to fly from Heathrow, as well as how critical Heathrow is for the UK’s trade routes and the risk to the economy of Britain relying on EU hubs which can close borders overnight. Heathrow will review its plans for expansion over the course of the next year.

Brexit

Following the UK’s departure from the EU on January 1st, 2021, flights can continue without disruption between the UK and EU. From a border perspective, the UK’s Border Operating Model outlines a phased approach for cargo to limit immediate changes at the UK border. Heathrow is working with the Government to deliver on their objective of ‘a world class border for people and goods’. As the UK’s biggest port by value and only hub airport, Heathrow has an integral role to play in helping the Government make ‘Global Britain’ a reality.

Outlook

Despite a slightly slower start to the year given the impact of Omicron, Heathrow maintains its passenger forecast of 45.5mn for 2022. The outlook for the adjusted EBITDA performance in 2022 also remains consistent with the guidance published in the Investor Report update on January 28th, 2022. Heathrow will continue to monitor passenger numbers and provide a further update at its 1Q results in April.

Heathrow does not forecast any covenant breach in 2022 under its current traffic scenario. Given the degree of ongoing uncertainty around traffic recovery, coupled with uncertainty in the final decision from the CAA on passenger pricing for the H7 regulatory period, Heathrow has also considered a severe but plausible downside scenario which models the interim tariff for 2022 and an overall H7 tariff at the lowest end of the range from the CAA’s Initial Proposals. Whilst this scenario is considered unlikely, a reduction in passenger numbers of over 8 million under the severe but plausible downside scenario is forecast to result, without further mitigation, in an ICR covenant breach at ADIF2 debt facility in December 2022. This uncertainty indicates the existence of a material uncertainty.

AGS (50%, equity-accounted) – UK

AGS response to COVID-19: AGS Airports continue to be significantly impacted by the unprecedented disruption to air travel following the spread of COVID-19 pandemic in March 2020 and subsequent emergence of new COVID-19 variants in 2021, although these restrictions eased with higher vaccination rates during 2H 2021. Overall, traffic was down by -89% in 1Q 2021 vs. 1Q 2020 while traffic in the last three quarters of 2021 improved by +173% vs. same period in 2020. The main focus of AGS during these times has been to ensure the health and safety of all its employees, business partners and airport passengers. AGS Airports have taken a number of health measures to provide a safe environment at the three airports.

AGS managed its cost base to face the current situation, including:

- Organizational transformation.

- Adoption of the Furlough Scheme until its completion on September 30th, both for employees and outsourced services.

- Rates waiver ratified by Scottish Parliament (Aberdeen & Glasgow).

- Contract renegotiation and volume related savings.

- Removal of all non-essential costs.

Capital expenditure has been deferred or cancelled, except for safety and compliance required investments.

Financial covenants: In June 2021, AGS completed negotiations regarding amending and extending its debt facility with unanimous approval from all lenders. Under the aforementioned agreement, AGS’s debt will mature in June 2024.

As part of the A&E, AGS ‘s shareholders committed to inject funds in a net amount of GBP70mn into AGS (GBP35mn total Ferrovial share), with an additional GBP30mn commitment (at 100%). There have been no further injections of the equity commitment in 2021.

Traffic: number of passengers increased by 6.2% (3.5mn passengers) driven by outperformance in Aberdeen and Glasgow, partially offset by underperformance in Southampton resulting from route suspensions and the Flybe collapse in 1Q 2020. Aberdeen traffic has been more resilient to COVID-19 vs other UK airports due to passengers related to Oil & Gas industry.

Revenues increased by +22.5% to GBP87mn driven by the outperformance in the last three quarters of 2021, particularly higher Commercial income, resulting from the reopening of commercial units to meet passenger demand, and other income, mainly in relation to COVID-19 testing income.

Operating Costs increased by +5.4% mainly due to COVID-19 testing costs, offset at EBITDA level with the aforementioned Covid testing income, end of Furlough scheme grant in Sep 21, and higher volumes partially offset by opex reduction initiatives implemented. Adjusted EBITDA was -GBP6mn (+66.7% vs 2020).

Following the successful A&E process in June, the cash position including Debt Service Reserve Account, amounts to GBP39mn as at December 31st, 2021.

AGS net bank debt stood at GBP716mn at December 31st, 2021.