-

1. Management Report 2021

- 1.1 In two minutes

- 1.2 Strategy and value creation

- 1.3 Ferrovial in 2021

- 1.4 Risks

- 1.5 Corporate Governance

- 1.6 Expected Business Performance in 2022

-

Appendix

- Alternative Performance Measures

- Sustainability Management

- Reporting Principles

- European Taxonomy

- Task Force on Climate Related Disclosures

- Scoreboard

- Contents of Non-Financial Information Statements

- SASB Indicators

- GRI Standard Indicators

- Appendix to GRI Standards Indicators

- Glosary of Terms

- Verification Report

-

2. Consolidated Financial Statements 2021

- Consolidated Financial Statements

- Audit Report

BUSINESS LINES

Toll Roads

407 ETR (43.23%, equity-accounted)

COVID-19

The Ontario Province has declared multiple stay-at-home orders, intermittent lockdowns and re-openings to help contain the spread of the new variants of the COVID-19. Additionally, the Government and employers have continued to recommend working-from-home when possible. The developments on COVID-19 related restrictions in 2021 for the Province are:

- Apr 8: Ontario Province entered in stay-at-home-order.

- Jun 2: stay-at-home order ended, since then, the region entered in a Reopening Plan based on vaccination rates & key public health care indicators. Provincial Gov. announced that remote learning will continue for the remainder of the school year.

- Jun 11: Step 1, focused on resuming outdoor activities with smaller crowds (up to 10 people).

- Jun 30: Step 2, with 70% of adults with 1st dose and 20% fully vaccinated. Further expands outdoor activities and limited indoor services (non-essential retail to 25% capacity).

- Jul 16: Step 3 (70-80% with 1st dose and 25% fully) expands access to indoor settings.

- Dec 19: additional health & safety measures in response to Omicron variant spread, 50% capacity in indoor settings and social gathering limits to 10 people indoors and 25 outdoors.

In January 2022, the Province announced a timeline for the gradual removal of these restrictions in February and March 2022.

The pandemic-related restrictions and resulting economic contraction continue to have an impact on demand for highway travel in the GTA. 407 ETR maintained strong liquidity with cash & cash equivalents as of December 31st, 2021 at CAD307mn and CAD800mn in undrawn credit facilities.

VKT (Vehicle kilometers travelled)

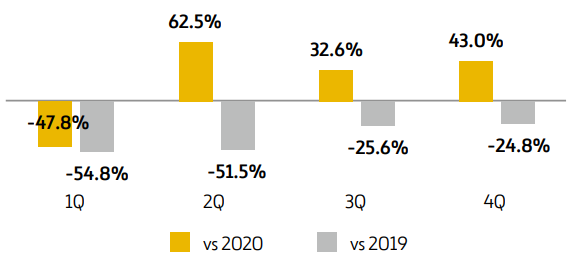

407 ETR experienced significant declines in traffic volumes on the back of COVID-19 impact, with stay-at-home orders and restrictions to mobility in effect for 1H 2021. Since 2Q 2021, traffic levels have been recovering notably as a result of the phased reopening of businesses, outdoor activities and public spaces across the Province. In 2021, VKTs increased by 13.0% vs 2020, on the back of Ontario Province moving into its 3rd stage of re-opening with additional restrictions being lifted (July 16th), along with the positive impact from schools reopening for in-person attendance in September. The recovery in any case has been dampened by employers’ decision to keep most of their workforce at home and the impact of Omicron variant in December, which forced the Province of Ontario to introduce additional public health, negatively impacting mobility.

Quarterly traffic performance

The Province declared the first Stay-at-Home order on March 17th, 2020, followed by intermittent lockdowns and re-openings; therefore, quarterly traffic performances in 2021 vs. 2020 are not entirely comparable.

While 407 ETR initially experienced significant declines in traffic since the onset of COVID-19 pandemic, a gradual improvement in traffic volumes has been observed throughout the year, even slightly in 4Q when traffic was impacted by new Omicron variant

Results for 100% of 407 ETR

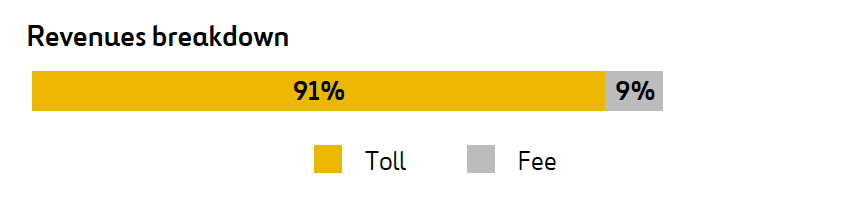

Revenues were up by +12.6% in 2021, reaching CAD1,023mn.

- Toll revenues (91% of total): +13.0% to CAD934mn, primarily due to improved traffic volumes compared to 2020, resulting from the relaxation of COVID-19-related restrictions. Average revenue per trip increased +4.6% vs. 2020.

- Fee revenues (9% of total) CAD89mn (+8.9%) due to the removal of the temporary suspension of lease fees, late payment charges during 2020, offset by lower volumes of License Plate Denial notification fees that were in place.

OPEX -2.7%, mainly due to lower customer operations costs resulting from a lower provision for lifetime expected credit loss, lower billing costs and lower collections costs.

EBITDA +16.1%, as a result of higher traffic volumes and revenues due the easing of pandemic related restrictions during 2021. EBITDA margin was 84.0% vs 81.4% in 2020.

Dividends: 407 ETR distributed CAD600mn in 2021 (CAD562.5mn in 2020). The dividends distributed to Ferrovial were EUR164mn in 2021).

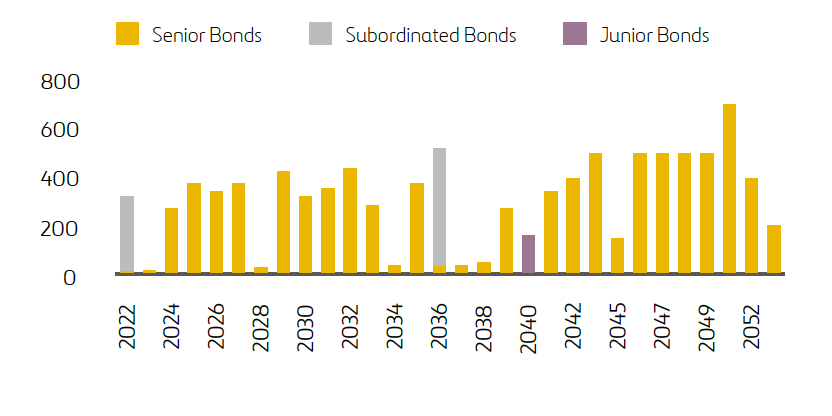

Net debt at end of December: CAD8,724mn (average cost of 4.11%). 54% of debt matures in more than 15 years’ time. Upcoming bond maturity dates are CAD319mn in 2022, CAD20mn in 2023 and CAD271mn in 2024.

407 ETR credit rating

- S&P: “A” (Senior Debt), “A-” (Junior Debt) & “BBB” (Subordinated Debt), with stable outlook, issued on 8 June 2021.

- DBRS: “A” (Senior Debt), “A low” (Junior Debt) & “BBB” (Subordinated Debt), all trends remain negative, issued on 17 June 2021.

407 ETR bond maturity profile

407 ETR Toll Rates

407 ETR Toll Rates

Toll rates have remained unchanged since February 2020, when 407 ETR implemented a new seasonal toll structure to address customer travel patterns and to manage overall traffic flow along 407 ETR, while optimizing its revenues. Given the impact of COVID-19, 407 ETR did not implement the changes included in the seasonal toll rates aside from the February 2020 increase.

Schedule 22

Due to the COVID-19 pandemic and related Province-wide shutdowns and stay-at-home orders, traffic on Highway 407 ETR has been significantly lower and minimum traffic thresholds cannot be achieved as prescribed under Schedule 22.

The COVID-19 pandemic is considered a Force Majeure event under the provisions of the Concession and Ground Lease Agreement, and therefore the 407ETR is not subject to Schedule 22 payments for 2020 and until the end of the Force Majeure event.

The 407ETR and the Province agreed that the Force Majeure event terminates when traffic in 407 ETR and adjacent roads reach pre-pandemic levels (measured as the average of 2017 to 2019), or when there is an increase in toll rates or user charges.

Upon the termination of the Force Majeure event, the 407ETR will be subject to a Schedule 22 payment, if applicable, commencing the subsequent year.

TEXAS MANAGED LANES (USA)

In 2021, traffic in the Texan Managed Lanes (MLs) was impacted by mobility restrictions until March 10th, when Texas fully reopened, along with adverse weather conditions, including winter storms in February (all three concessions were closed for 7 days) and heavy rain during May (which was 60% more than the average of May 2020), and surges in COVID-19 cases during the summer as well as in December (Omicron variant).

Currently, there is no major COVID-19 related policy that directly relates to mobility. As of December 31st, 2021, in Dallas-Fort Worth fully vaccination rate ranges at 55% – 66% (accounting for all residents including children).

There has been a sustained recovery since the reopening, with traffic showing slowdowns as COVID-19 cases registered spikes in Texas in August and December, the later due to the Omicron variant. Nevertheless, traffic has shown a solid recovery. NTE 35W traffic was above pre-pandemic levels (2019) in 2021 (+9.0%) while NTE performed in line with 2019 (-0.8%). LBJ kept improving but still below (-23.8% vs. 2019). All MLs posted solid avg. revenue per transaction NTE 35W +15.6%, NTE +13.4% & LBJ +4.6%.

NTE 1-2 (63.0%, globally consolidated)

In 2021, traffic increased by +32.7%, already reaching the same traffic levels of 2019 (pre-COVID-19), following a strong recovery since 2Q given the full reopening in Texas since mid-March, partially offset by the severe weather conditions in February and May and the impact of surges in COVID-19 cases during the summer and in December. Since 2Q, NTE registered the same or more monthly mandatory mode events than in February 2020 (pre-COVID-19). Additionally, the midday traffic volumes and PM peaks at NTE are already higher than pre-COVID levels.

The average toll rate per transaction reached USD5.6 vs. USD4.9 in 2020 (+13.4%) positively impacted by higher proportion of heavy vehicles (toll multiplier 2x – 5x) and higher toll rates. This led to Revenues reaching USD187mn or +50.0% vs. 2020.

EBITDA reached USD164mn (+54.3% vs. 2020). EBITDA margin of 87.4% (85.0% in 2020).

NTE EBITDA EVOLUTION

Dividends: NTE distributed two regular dividends in June and December, for a total of USD100mn (EUR53mn FER’s share). In 2020, NTE distributed USD46mn dividend (EUR25mn FER’s share).

NTE net debt reached USD1,223mn in December 2021 (USD1,232mn in December 2020), at an average cost of 4.12%.

LBJ (54.6%, globally consolidated)

In 2021, traffic increased by +23.0%, on the back of a steady recovery since 2Q given the full reopening in Texas in mid-March, partially offset by the severe weather conditions in February and May, and the impact of surges in COVID-19 cases during the summer and in December.

The average revenue per transaction reached USD3.6 in 2021 vs. USD3.4 in 2020 (+4.6%) positively impacted by higher proportion of heavy vehicles (toll multiplier 2x – 5x) and higher toll rates. This, together with higher traffic led to Revenues reaching USD133mn (+27.3% vs. 2020).

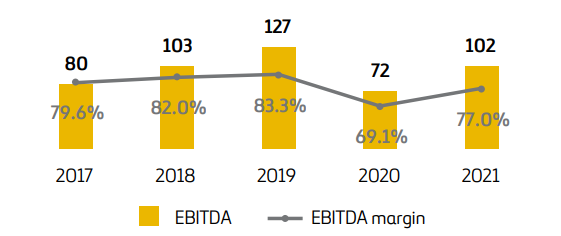

EBITDA reached USD102mn (+42.0% vs. 2020) with an EBITDA margin of 77.0% (69.1% in 2020).

LBJ net debt was USD1,998mn in December 2021 (USD1,660mn in December 2020), at an average cost of 4.03%.

In December 2021, LBJ completed the issuance of USD609mn of 2021 senior secured notes, which proceeds will be used to repay a portion of the project company’s outstanding TIFIA loan (USD300.6mn) and fund an equity distribution to the project sponsor (USD300.6mn). The cost of new debt was lowered to 3.797% yield to maturity (vs 4.22% TIFIA coupon) & maturity of overall debt structure ascends to 2057 (vs. 2050 prev). The transaction costs were USD7mn.

Dividends: LBJ distributed USD360mn dividends in 2021 following the issuance of USD609mn secured notes in Dec. 2021 (EUR167mn FER’s share vs EUR109mn in 2020). In 2020, LBJ distributed its first dividend (USD229mn) after five years of operation.

NTE 35W (53.7%, globally consolidated)

In 2021, NTE 35W traffic increased by +26.8% reaching traffic figures above pre-COVID-19 levels given the positive effects of ramp-up and heavy vehicles resilience along with the solid recovery since 2Q given the full reopening in Texas since mid-March, partially offset by the severe weather conditions in February and May and the impact of surges in COVID-19 cases during the summer and in December.

Average revenue per transaction was USD4.0 in 2021, vs. USD3.5 in 2020 (+15.6%), positively impacted by higher proportion of heavy vehicles (toll multiplier 2x – 5x) and higher toll rates. These, together with traffic increase, led to Revenues reaching USD142mn (+45.3% vs. 2020).

EBITDA reached USD119mn (+46.1% vs. 2020) with an EBITDA margin of 83.9% (vs 83.4% in 2020).

NTE 35W net debt reached USD1,055mn in December 2021 (USD915mn in December 2020), at an average cost of 4.85%, including NTE 3C.

NTE 3C (53.7%, globally consolidated-under construction)

- Development, design, construction & operation of Seg. 3C, including the construction of 2 managed lanes in each direction and the reconstruction of existing general-purpose lanes.

- Flexible Pricing Framework: freedom to set toll rates under a soft cap & 2x-5x heavy vehicles multiplier (3x avg)

- Length:6.7miles northbound extension of NTE 35W 3A & 3B (operating since 2018)

- Concession term: 2061

- Opening to traffic expected by end of 2023

- Operation & Maintenance and toll collection: exclusive right and obligation to operate, maintain, repair and collect tolls. Tolls collected by North Texas Tollway Authority are in line with tolling agreement with TxDOT. TxDOT assumes collection risk.

I-77 (65.1%, globally consolidated)

North Carolina lifted all restrictions, including the mask mandate in most circumstances, on May 14th. North Carolina experienced in September the highest number of new COVID-19 cases since February however, as the cases subsided in October, traffic returned quickly.

In 2021, traffic increased by +45.8% as the state has been easing mobility restrictions throughout the period. The traffic reached pre-COVID-19 levels by the end of June.

The average revenue per transaction was USD1.2 in 2021 vs. USD0.8 in 2020 (+46.5%).

Revenues reached USD36mn (+102.1% vs. 2020) as a result of the traffic returning quickly as COVID-19 trends improved.

EBITDA reached USD20mn with an EBITDA margin of 54.9% (24.9% in 2020).

I-77 net debt was USD263mn in December 2021 (USD272mn in December 2020), at an average cost of 3.67%.

Credit rating

| PAB | TIFIA | |

|---|---|---|

| FITCH | BBB- | BBB- |

| DBRS | BBB | BBB |

I-66 (55.7%, globally consolidated-under construction)

Ferrovial acquired an additional 5.704% in I-66, increasing its stake to 55.704%. The value of the transaction accounts to EUR162mn, along with EUR36mn as part of its commitment of additional equity injections until the completion of construction corresponding to that 5.704%. The acquisition of control of the concession company implies the recognition of a positive fair value adjustment before deferred taxes for Ferrovial of EUR1,117mn, as the previously acquired 50% stake has to be valued at fair value. Additionally, by taking control of the concession company, the complete project debt is integrated into Ferrovial’s consolidated balance sheet, that reaches EUR1,511mn as of December 31st, 2021.

IRB

Ferrovial, through its subsidiary Cintra, acquired 24.86% of the shares of the Indian listed company IRB Infrastructure Developers Ltd for EUR369mn. The deal has been completed (On Dec. 29th) after a preferential share issue by IRB Infrastructure Developers, following the approval by IRB’s Shareholders’ Meeting and after obtaining the pertinent statutory approvals. IRB is a leading player in the Indian market, where it manages 23 projects and around 2,000 kilometers of toll roads. As a result, Ferrovial is now a significant minority shareholder with representation on the company’s Board of Directors. Cintra will support the company’s development and share its extensive international experience in managing toll roads and analyzing new investment opportunities. IRB will continue to be managed by its majority shareholder, Virendra D. Mhaiskar (his family and holding company).

On February 12th, 2022, Fitch Ratings upgraded the International Long-Term Issuer Default Rating on IRB Infrastructure Developers Limited’s to ‘BB+’ from ‘BB’, and removed the rating from Rating Watch Positive. The Outlook is Stable. The upgrade of the rating on IRB reflects improvement in its financial profile after the equity injection made by Ferrovial and GIC.

El 12 de febrero, Fitch Ratings elevó la calificación crediticia de IRB Infrastructure Developers Limited a ‘BB+’ desde ‘BB’ y eliminó la calificación de Rating Watch Positive. La perspectiva es estable. El incremento del rating de IRB refleja la mejora de su perfil financiero tras la inyección de capital realizada por Ferrovial y GIC.

OTHER TOLL ROADS

Ferrovial’s portfolio includes a number of toll roads which are, mainly, availability projects located in countries with low government bond yields (Spain, Portugal and Ireland) and long duration. Among the availability projects with no traffic risk or equivalent to availability projects held by Ferrovial are: A-66, Algarve (until sale completion), M3, M8 and Toowoomba.

- Spain: traffic in 2021 was impacted by the restrictive measures adopted by local governments to face the pandemic. However, since late April, traffic improved as Catalonia and Andalusia lifted their regional lockdowns. Traffic was also positively impacted by the preference for domestic destinations during summer holidays and a strong vaccination rate, resulting in lower COVID-19 cases. Autema’s traffic was more impacted than Ausol by the Omicron variant as the Catalonian government imposed some mobility restrictions in December. When compared to 2019, pre-pandemic levels, traffic in Autema was -18.1%, while traffic in Ausol I and Ausol II was -17.6% and -20.1%, respectively.

- Portugal: on January 15th, 2021, a new lockdown was approved that was in place for the entire 1Q. Since the end of March, mobility restrictions started to ease, with the State of Emergency lifted on April 30th and traffic recovering since then. Since August, traffic recovery was steeper as all the mobility measures were lifted and vaccination pace was extremely fast. In Azores, the regional government has been applying selective lockdowns depending on the virus evolution of each municipality. At the end of December, traffic was impacted by compulsory work-from home imposed by the Government given the expansion of the Omicron variant. In 2021, traffic decreased -15.2% in Algarve and +0.8% in Azores, when compared to 2019.

- Ireland: On December 24th, 2020, the government approved the maximum level of restrictions, which was in place for the entire 1Q. During 2Q, there was a steady process of reopening, which translated in improving traffic trends. In November, traffic volumes were close to 2019 levels. In December, traffic was not materially affected by the Omicron variant as major restrictions were not implemented. In 2021, M4 was down -11.3% and -10.5% in M3, when compared to 2019.